Explanatory Notes – Guide on Delegation of Authority

For questions or comments, please contact us :

NC-CFOB-Financial_Policy_Questions_Politique_Financière-GD

Last revision: December 2009

Please Note: This policy/document is currently under review and is being updated to reflect new procedures and terminology associated with the implementation of myEMS (SAP)

- INTRODUCTION

- TYPES OF FINANCIAL SIGNING AUTHORITIES

- DELEGATION CHART - SPECIFIC CONSIDERATIONS

- DELEGATION CHART - FINANCIAL AUTHORITIES - OPERATING FUNDS

- Area of Authority (Column 1)

- Commitment Authority (Column 2)

- Inter-Departmental Arrangements and Arrangements with Other Federal Institutions (Column 3)

- Inter-Governmental Arrangements and Arrangements with Provincial Entities (Column 4)

- Requisition Authority - Goods, Services and Construction (Column 5)

- Project authority (Column 6) – some restrictions apply

- Claims against the Crown (Columns 7 to 10)

- Conferences (Column 11) – some restrictions apply

- Ex Gratia (Column 12)

- Hospitality (Column 13) – some restrictions apply

- Membership Fees (Column 14) – some restrictions apply

- Recognition

- Relocation (Column 17) – some restrictions apply

- Isolated Post & Government Housing (Column 18) – some restrictions apply

- Staffing Action, Extra Duty (Column 19)

- Standing Advances (Column 20)

- Training/Tuition (Column 21)

- Travel (Column 22)

- Contracting Authority (Column 23) – some restrictions apply

- Leasing Authority (Column 24) – some restrictions apply

- FAA Section 34 Contract Performance (Column 25)

- FAA Section 33 Payment Authority (Column 26)

- DELEGATION CHART - SPECIAL FINANCIAL AUTHORITIES

- Accept and Release Security Deposit (Column 1)

- Bid/Contract Security (Column 2)

- Cash Loss Charge-Off to Appropriation (Column 3)

- Cheque Issue Regulation - DBA (Column 4)

- Deduction and Set-Off of Accounts - (Column 5 to 7)

- Garnishee Approval (Column 8)

- Authority to Fix Travel and Living Expenses of PAB Temporary Members (Column 9)

- Refund of Revenue (FAA s.20) (Column 10)

- Transaction Against the Annuities Account (Columns 11 and 12)

- Transaction Against the Civil Service Insurance Account (Columns 13 and 14)

- Transaction - Annuities Agent (Columns 15 and 16)

- Write-Off of Crown Assets (Column 17)

INTRODUCTION

These explanatory notes are companion to the Delegated Authorities Manual.

These explanatory notes are meant to provide guidance only and management should not rely solely on them when making a decision. Always consult the appropriate policies and legislations in force in this regard.

These notes refers to the policies and procedures required for the administration of Financial Signing Authorities and provide an understanding on the different types of Financial Signing Authorities the requirements of Section 32, 33, and 34 of the Financial Administration Act, the Restrictions and how to interpret the Financial Signing Authorities Charts (Delegation Instruments).

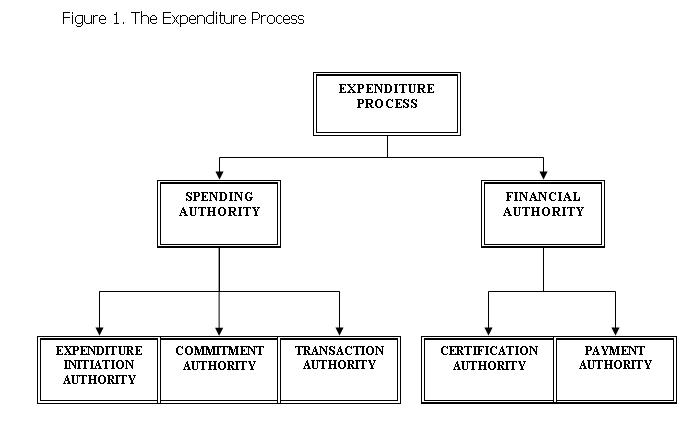

Financial Administration Act (FAA), central agency policies, grants and contributions program terms and conditions and other acts, regulations and policies allow financial signing authorities and other authorities associated with the Expenditure Process (Fig.1) to be delegated to departmental/commission officers and other bodies by the Minister of Human Resources and Skills Development, the Minister of Labour, the Deputy Minister/Chairperson of the Commission. These authorities are incorporated in the delegation instruments.

The authorities referred to in these instruments are delegated to maximum dollar limits and to position titles at organizational levels in accordance with central agency and Human Resources and Skills Development Canada (HRSDC) administrative policies.

The financial signing authorities may also be subject to lower limitations imposed in specific circumstances by executive order or on the instruction of the Minister. All maximum limitations indicated are general limitations, and lower limitations may be imposed on a local basis, where desirable, at the discretion of the Responsibility Centre Manager (RCM ) or supervisor.

The incumbent of the position with delegated authority must follow all relevant policies and procedures aligned with managerial, budgetary and operational responsibilities and apply signing authority within the area of authority designated.

Signing authorities carry with them the responsibility for ensuring that all the related managerial and financial controls are effectively enforced and that all the normal requirements of probity and prudence are observed. Personnel authorized to exercise signing authority will be held accountable for all expenditures of public funds for which they are responsible. A number of principles apply in the exercising of delegated authorities for financial administration. They are described below.

Authorities are delegated to positions, not to individuals identified by name. Delegated authority cannot be redelegated, i.e. a person who has been appointed to a position with delegated authority may not redelegate the authority to another position or person. Furthermore, a person who does not have the delegated authority may not sign on behalf of an individual who does (i.e. over a superior’s signature block) unless in an acting situation.

The delegation instrument indicates the lowest levels to which signing authorities are given. This means that all positions in the hierarchical order above this position also have at least this same delegation (some exceptions may apply).

The Area of Responsibility indicated in the delegation instrument is a key limitation in the exercise of delegated authorities. A delegation by the Minister and DM does not eliminate the responsibility of RCM s to establish efficient control procedures within that person’s area of responsibility. The delegation sets the lowest level of position at which financial authority may be exercised, and additional limitations may need to be imposed in order to meet local requirements for effective control.

RCMs, through the prudent use of their delegated authorities, will be accountable for effectively and efficiently managing their resources and related deliverables in accordance with the Financial Administration Act, Treasury Board (TB), other central agencies and departmental regulations, policies and directives. Persons to whom authorities for financial administration have been delegated are responsible for ensuring that they understand the extent of their authority and financial accountability. Personal Benefit

No person shall exercise either payment or spending authority with respect to a transaction from which that person can personally benefit, such as expenditures for travel, relocation, hospitality, reimbursement of tuition fees, or membership dues. Furthermore, every person involved in a transaction which results in a personal payment must have the expenditure initiation portion of that transaction authorized by the person’s superior officer

No person occupying a position on an acting basis shall exercise the financial authorities given to that position unless properly authorized in writing by an officer to whom the normal incumbent of the position reports. Although it may be sufficient under some circumstances for the incumbent to simply provide his/her superior with notification of the acting appointment, if the individual acting in the position is expected to exercise financial signing authorities, the more senior superior must provide written authorization. Please refer to Policy on Delegation of Financial Signing Authorities and Specimen Signatures.

Authority to confirm performance and price under Section 34 of the FAA, and payment authority under Section 33 of the FAA must not be exercised by the same individual with respect to a particular payment. This principle recognizes the need for a division of duties to maintain financial probity. Persons with delegated signing authority may exercise either spending or payment authority, but not both.

Further division of responsibility for expenditure initiation, commitment authority, transaction authority and confirmation of contract performance and price is an effective means of preventing the possibility of error or fraud. It is recognized however that there is a trade-off between risk and efficiency and this will determine the degree to which these functions are kept separate.

Authorities for financial administration delegated to a position must be withdrawn by the superior of the position and/or by CFOB, if it is determined that the delegated authorities are being abused. Where delegated authorities are inadvertently exercised incorrectly, as a minimum there is a requirement for closer monitoring, which may include probationary periods. Authorities can be reinstated when the superior and/or CFOB is satisfied that the situation has been corrected and the abuse or improper use will not re-occur.

Annual Review of Signing Authority

A periodic review of signing authorities must be made to determine their continuing validity. This review must be conducted by CFOB in consultation with program branches to ensure that the types and levels of authorities delegated are in accordance with the department’s organizational structure and operational requirements. Delegated authority holders will be asked to review the specimen signature cards pertaining to their areas of responsibility.

TYPES OF FINANCIAL SIGNING AUTHORITIES

The following explains the types of Financial Signing Authorities associated with the expenditure process and their place in the expenditure cycle. It should be noted that the current departmental delegation of authority chart for operating funds does not fully reflect the Expenditure Process as shown in the TB Directive on Delegation of Financial Authorities for Disbursements.

The Expenditure Process (i) consists of two authorities:

1-Spending Authority (ii):

Consists of three main elements: Expenditure Initiation Authority, Commitment Authority under S32 of the FAA and Transaction Authority.

(i) The concept of Expenditure Process was introduced by Treasury Board’s Directive on Delegation of Financial Authorities for Disbursements (dated October 1, 2009) which replaces the Policy on Delegation of Authorities (dated December 1, 1993)

(ii) Under the Policy on Delegation of Authorities (dated December 1, 1993), Spending Authority consists of Expenditure Initiation, Commitment Authority, Contracting Authority, and Confirmation of Contract Performance (i.e. FAA s.34)

2-Financial Authority (iii):

Financial Authorities are divided into two main categories: Certification Authority and Payment Authority.

(iii) Under the Policy on Delegation of Authorities (dated December 1, 1993), Financial Authority consists of Spending Authority and Payment Authority (i.e. FAA s.33)

Expenditure Initiation Authority

This is the first step in the expenditure cycle and occurs when a Manager decides to acquire goods or services which will eventually result in an expenditure against his budget. Some examples are; the decision to hire employees, to order supplies or services or to authorize travel. The authority lies with managers responsible for budgets.

Commitment Authority

This is the second step in the expenditure cycle. This authority confirms that there are sufficient funds available in the appropriation to cover the proposed expenditure.

The authority to confirm the availability of funds before a contractual arrangement is entered into under section 32 of the FAA. Specific FAA wording is as follows:

32(1) “No contract or other arrangement providing for a payment shall be entered into with respect to any program for which there is an appropriation by Parliament or an item included in estimates then before the House of Commons to which the payment will be charged unless there is a sufficient unencumbered balance available out of the appropriation or item to discharge any debt that, under the contract or other arrangement, will be incurred during the fiscal year in which the contract or other arrangement is entered into.”

32(2) “The deputy head or other person charged with the administration of a program for which there is an appropriation by Parliament or an item included in estimates then before the House of Commons shall, as the Treasury Board may prescribe, establish procedures and maintain records respecting the control of financial commitments chargeable to each appropriation or item.”

Transaction Authority (iV)

The authority to enter into contracts or sign-off on legal entitlements. A contract is an agreement between a contracting authority and an individual or firm to provide a good, perform a service, construct a work, or lease real property. The contract document describes the subject of the transaction, the price and conditions agreed upon and the time within which the goods or services are to be delivered. As specified by the Treasury Board Contracting Policy, there are four basic types of contracts: goods contracts; service contracts; construction contracts; and accommodation leases.

(iv) Same as Contracting Authority under the Policy on Delegation of Authorities (dated December 1, 1993).

Certification Authority

This is the third step in the expenditure cycle. It confirms that the work has been performed as required, services and supplies have been satisfactorily provided, travel and relocation have been successfully carried out, employees have worked overtime and contract performance has been in accordance with contract arrangements and conditions. It is also used for Grants and Contributions to confirm that the terms and conditions of the particular program have been carried out.

This authority is delegated by the Minister to appropriate officers to certify under section 34 of the FAA. In some circumstances, authority to certify contract performance under section 34 of the FAA is delegated to positions outside of the responsibility centre in common servicing arrangements. Such delegation is appropriate when invoices are received centrally and when it is feasible to accumulate centrally commitment, receiving, inspection and other documentation feasible to certify performance and prices without further reference to the responsibility centre manager. Specific FAA wording is as follows:

34(1) “No payment shall be made in respect of any part of the public service of Canada, unless, in addition to any other voucher or certificate that is required, the deputy of the appropriate Minister, or another person authorized by that Minister, certifies:

(a) in the case of a payment for the performance of work, the supply of goods or the rendering of services:

- that the work has been performed, the goods supplied or the service rendered, as the case may be, and that the price charged is according to the contract, is reasonable,

- where, pursuant to the contract, a payment is to be made before the completion of the work, delivery of the goods or rendering of the service, as the case may be, that the payment is according to the contract, or

- where, in accordance with the policies and procedures prescribed under subsection (2), payment is to be made in advance of verification, that the claim for payment is reasonable, or

(b) in the case of any other payment, that the payee is eligible for or entitled to the payment.”

34(2) “The Treasury Board may prescribe policies and procedures to be followed to give effect to the certification and verification required under subsection (1).”

Payment Authority

This authority is the fourth and final step in the expenditure cycle and is given primarily to Financial Officers to requisition payments against the proper appropriation. Payment authority is exercised after the review of the legality of payments and exercising all appropriate financial controls.

This authority is delegated by the Minister primarily to financial officers under section 33 of the FAA. This delegation ensures that all payments and all other charges requisitioned against the Consolidated Revenue Fund are timely, properly authorized and legal as prescribed by the Policies on Account Verification and Payment Requisitioning.

The objective of establishing payment authority in accordance with this definition is to ensure that all the statutory and regulatory requirements for the control of funds and the requisitioning of payments are met. Due to the need for independent control, payment authority under section 33 should be vested with financial officers under the functional direction of the Chief Financial Officer.

Specific FAA wording is as follows:

33(1) “No charge shall be made against an appropriation except upon the requisition of the appropriate Minister of the Department for which the appropriation was made, or of a person authorized in writing by that Minister.”

33(2) “Every requisition for a payment out of the Consolidated Revenue Fund shall be in such form, accompanied by such documents and certified in such manner as the Treasury Board may prescribe by regulation.”

33(3) “No requisition shall be made pursuant to subsection (1) for a payment that:

- would not be a lawful charge against the appropriation;

- would result in an expenditure in excess of the appropriation; or

- would reduce the balance of the appropriation so that it would not be sufficient to meet the commitments charged against it.”

33(4) “The appropriate Minister may transmit to the Treasury Board any requisition with respect to which that Minister desires the direction of the Board, and the Board may order that payment be made or refused.”

DELEGATION CHART- SPECIFIC CONSIDERATIONS

Positions Titles/Reporting Levels

Listed down the left side of the chart are the position titles to which the various authorities have been delegated. Some of these positions are generic titles. Not every Supervisor, for instance, has financial signing authority. The RC Manager must determine his organization structure and who should have the required signing authority in conjunction with this chart.

Positions are described in specific terms as shown on the official departmental organization charts (e.g., Deputy Minister and Chairperson/Assistant Deputy Minister, Human Resources) or in generic category terms (e.g., Director General/Director).

The authorities delegated to the positions named in the delegation instruments are applicable to the incumbents in the positions and persons appointed or designated to act in the absence of the incumbents.

- An Executive Head position represents all Assistant Deputy Ministers, or equivalent positions, at National Headquarters and in the regions. An Executive Head is an organizational position at a senior executive level which reports directly to the Deputy Minister and Chairperson or the Associate Deputy Minister and Vice-Chairperson.

- A Responsibility Centre Manager (RCM) is a position which reports directly or indirectly (through several organizational levels) to the Minister, Deputy Minister and Chairperson, Associate Deputy Minister and Vice-Chairperson or Executive Head. An RCM is responsible and accountable for budgetary and human resources and is represented by positions such as Director General (reporting to Executive Head), Director, Manager, Chief, etc. Some RCM positions may report directly to the Deputy Minister or to the Associate Deputy Minister in their line of responsibility as support officers. These positions are not considered as Executive Heads, because of their reporting relationship: they are not part of the senior executive group.

- A Director/Manager, Service Canada Centre (SCC), is the Director at the EX-1 or PM-6 classification level (parent office) and the Manager at the PM-5 or PM-4 classification level located in a parent or satellite office.

- A position at an organizational level reporting to a superior position is represented by various position titles depending on the organization. In most cases, the positions at the first/second/third, etc. levels are "officers" with sufficient responsibility to assist the superior position in the administration of a responsibility centre and program delivery. However, circumstances may require that positions such as clerical and administrative assistant (i.e. non-officers), at the appropriate reporting levels with delegated authority, exercise authority for particular financial functions. The accountability for the function, however, remains with the position with budgetary responsibility.

- With regard to the Financial Signing Authorities - Operating Funds, positions in the "Operational" activities are those responsible for the management of the responsibility centres or assisting in the management to facilitate efficient and timely processing of financial responsibilities. Positions in the "Corporate" activities are those responsible for providing or assisting in the provision of common services for the benefit of all RCMs and as an efficient means of transacting a required financial activity or as a requirement of a central agency policy.

- Financial Officers and section 33 of the FAA. The level and designation of the financial officer, as it relates to signing section 33, can be variable and would be dependent on the volume and number of locations where this function is required. In cases where there are multiple locations and numerous requirements for sign-off having CR-05s or AS-1s in place could be viable, provided they have the appropriate level of experience. In addition it is possible the position could be within the Operations Branch with functional direction from CFO.

- A Financial Officer * is defined as a person who has been trained and appointed to administer financial functions and duties, above the clerical level, regardless of his or her formal job classification. For example, a person that is classified in personnel administration (PE) can carry out the role of a financial officer if he or she has the requisite education and training. Financial officers are under the functional direction of the Chief Financial Officer.

* Definition currently under review

The symbols (letters and numbers) indicate the maximum dollar amount of limitations on signing authorities.

"F" (FULL) indicates full authority within budgetary limits;

All delegated authority (full and dollar amount limits) is subject to departmental/commission and central agency policy limitations and conditions, to grants and contributions programs’ terms and conditions limits and to budgetary limits of the area of responsibility (reference should be made to the "Restrictions" section in the Delegated Authorities Manual as well as other conditions noted in other departmental manuals and documents and Treasury Board policy and directive announcements).

Treasury Board policy specifies that in most cases, delegated authorities to positions may be restricted by geographical location, organizational unit, operational activity and dollar amounts commensurate with the duties and responsibilities of positions. Delegation restrictions are located within the Delegated Authorities Manual. Through the Delegation of Financial Signing Authorities and Specimen Signature Card, RC Managers can impose further restrictions in order to meet local requirements for effective control.

DELEGATION CHART - FINANCIAL AUTHORITIES – OPERATING FUNDS

This delegation chart is for authorities related to operating funds (also known in the past as operating and maintenance, i.e. O&M funds).

Operational and corporate service activities take place within an area of responsibility. The area of responsibility can range from the entire department/commission to a responsibility centre. The area of authority encompasses the responsibility centre operations for which an incumbent of a position is responsible and accountable or is assisting in the responsibility. The Department/Commission area enables authority to be exercised for any national location. The Region area also includes regionally managed NHQ RCs.

(example to follow)

With regard to authority for grants and contributions programs, special authorities and transactions against the Employment Insurance and Annuities accounts, the area of authority represents the activity for which the position has been assigned responsibility or for which the position is providing assistance in the accomplishment of the activity.

Commitment Authority (Column 2)

Is the authority to carry activities or functions related to the control of commitment as required by section 32 of the FAA. Commitment authority is the authority delegated by the Deputy Minister to certify, prior to entering into a commitment, that sufficient funds are available to discharge the expenditure at some future time.

Officers who are delegated payment authority rely on these records to meet their responsibility, under section 33(3) (c) of the FAA, to ensure that no balance of an appropriation will be reduced to the point where it is insufficient to meet all the commitments charged against it.

It should be noted that according to the Delegation of Authority Instrument, section 32 is delegated to the CFO/Comptrollers only. Although section 32 is only delegated to the CFO/Comptrollers, the procedure for Commitment Control is exercised by officers in the Corporate Management System (CMS). Commitment Control is provided through the maintenance of budgetary control records in CMS. Since section 32 is not broadly delegated to managerial positions, specimen signature cards do not reflect section 32 authorities.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to the Directive on Delegation of Financial Authorities for Disbursements

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=17060

Refer to Directive on Expenditure Initiation and Commitment Control

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=17061

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

Human Resources and Skills Development Canada

Refer to the O&M Policy

http://intracom.hq-ac.prv/en/cfob/policies/standard_om.shtml

Inter-Departmental Arrangements and Arrangements with Other Federal Institutions (Column 3)

This is the authority to enter into agreements with other federal government departments, agencies and Crown corporations for the provision of goods and services.

Memorandum of Understanding (MOU) is used to refer to agreements between federal government departments /agencies that may or may not have financial obligations. They could more usefully be called an Inter-Departmental Arrangement. A Memorandum of Understanding between federal departments that transfers funds should look much like a formal contract, with clear financial information, performance indicators, accountability mechanisms, audit, etc.

Non-monetary transactions are exchanges of non-monetary assets, liabilities or services for other non-monetary assets, liabilities or services.

Cost-shared projects, where a government program cooperates with another party toward a common goal, are not considered to be non-monetary transactions.

Arrangements between departments:

- Includes Crown corporations

- Can contain a wide range of activities

- May be of direct use and benefit by departments

- Supports operations and/or meet program objectives

- Are considered not legally enforceable as both departments are part of the Government of Canada

Special Provisions for Courses with Canada School of Public Service (CSPS):

All training currently taken through the CPS requires an Interdepartmental Letter of Agreement (ILA). The approval authority for ILAs (under Inter-Departmental Arrangements and Arrangements with Other Federal Institutions (Column 3)) is restricted to DG level and Director CFOB. The purpose of this delegation is to ensure the department has control over substantive expenditures or commitments of departmental resources made through inter-departmental arrangements.

To facilitate the efficient authorization of training, the Chief Financial Officer of HRSDC has authorized the following:

- For individual employee training, the delegation for Training/Tuition (column 21) is the delegation to utilize for approving both the training and the ILA.

- For group training up to $5,000, the delegation for Training/Tuition (column 21) is the delegation to utilize for approving training, but the ILA must be approved at the Director level or above.

- For group training over $5,000, the delegation for Training/Tuition (column 21) is the delegation to utilize for approving training and the delegation for Inter-Departmental Arrangements and Arrangements with Other Federal Institutions (Column 3) is the delegation to utilize for approving the ILA.

Note that all processes in place from the Service Canada College and branch/regional management must be respected.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to the Policy on Accounting for Non-Monetary Transactions

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12173

Refer to the Contracting Policy

http://www.tbs-sct.gc.ca/pubs_pol/dcgpubs/contracting/contractingpol_e.asp

Inter-Governmental Arrangements and Arrangements with Provincial Entities (Column 4)

Arrangements between Human Resources and Skill Development Canada and provincial entities, which transfer money or property, should properly be referred to as Inter-Governmental Arrangements (IGA). Although such arrangements may be negotiated outside the government contract regulations, they should include most of the clauses that appear in government contracts in order to provide appropriate financial and program accountability.

Contracts with third parties outside government are entered into in accordance with the Government Contract Regulations (GCRS) and the Treasury Board Contracting Policy.

Arrangements between departments and other levels of government:

- Includes universities and hospitals

- Wide range of activities

- May be of direct use & benefit by departments, other levels of government and/or Canadians and/or program target groups

- To support operations and/or achieve program objectives

- May be legally enforceable; consult your legal counsel

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to the Policy on Accounting for Non-Monetary Transactions

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12173

Refer to the Contracting Policy

http://www.tbs-sct.gc.ca/pubs_pol/dcgpubs/contracting/contractingpol_e.asp

Requisition Authority - Goods, Services and Construction (Column 5)

Delegation of Authority to enter into a contract to acquire goods and services and to carry-out construction. Library books, technical and professional texts and publications, subscriptions and renewals is granted to the Minister from the Minister of Public Works and Government Services (PWGSC).

May be further subdivided into “Internal Requisitions” where authority is required to request the receipt of supplies/services from a Central Administration Branch within NHQ and “Requisition to Central Agencies” where authority is required to issue purchase orders to centralized government agencies (i.e. PWGSC) for the provisions of goods or services.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to the Contracting Policy

http://www.tbs-sct.gc.ca/pubs_pol/dcgpubs/Contracting/contractingpol_e.asp

Refer to Directive on Acquisition Cards

Project authority (Column 6) – some restrictions apply

The Treasury Board Policy on the Management of Projects defines a project as “an activity or series of activities that has a beginning and an end. A project is required to produce defined outputs and realize specific outcomes in support of a public policy objective, within a clear schedule and resource plan. A project is undertaken within specific time, cost and performance parameters.”

The approval authority will establish an agreed upon project baseline when approving the project. Any significant deviations from this baseline must be authorized by the appropriate approval authority.

Other Reference Material

Refer to the Project Approval Policy

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12075

Refer to the departmental Project Restrictions Document

hyperlink not available yet

Claims against the Crown (Columns 7 to 10)

A claim against the Crown is a request for compensation that is settled in or out of court for monetary compensation to, or indemnity for, the loss, detriment, or injury of the claimant.

Claims are defined as “requests for compensation to cover losses, expenditures, or damages sustained by the Crown or a claimant, including requests or suggestions that the Crown make an ex gratia payment. They can be settled in or out of court.

A liability claim is a recognized liability at which the Crown is at fault. The claimant must provide a statement of facts on the claim at the earliest reasonable opportunity. A release is required in the case of a liability payment.

The Deputy Minister shall make every reasonable effort to obtain satisfaction of claims by the Crown, taking into account administrative expediency and cost-effectiveness.

For claims by and against servants of the Crown, the department must ensure that the indemnification and legal assistance policies are considered at the earliest opportunity.

Claims against the Crown – Other out-of-court settlements (Column 7)

To authorize and sign an out-of-court settlement of a claim payment where it includes claims for damages. It does not include claims in a contract, claims under Section 11 of the Canadian Human Rights Act (Equal Wages), or claims governed by other authorities such as losses and recovery of money, damages to servants' effects on relocation or the travel policy.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Policy on Legal Assistance And Indemnification

Archived [2008-09-01] - Policy on the Indemnification of and Legal Assistance for Crown Servants

Refer to the Directive on Claims and Ex Gratia Payments

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15782

Human Resources and Skill Development Canada

Refer to the Policy on Claims and Ex gratia Payments

Claims against the Crown – Court Awards (Column 8)

Authority to authorise payment of a claim obtained by a claimant through a Court Award.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Directive on Claims and Ex Gratia Payments

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15782

Human Resources and Skills Development Canada

Refer to the Policy on Claims and Ex gratia Payments

Claims against the Crown – Out-of-court settlements for motor vehicle accidents claims (Column 9)

To authorize and sign an out-of-court settlement of a claim payment where Crown-owned vehicles are involved in motor vehicle accidents and where a legal opinion has been obtained recommending payment.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Policy on Legal Assistance and Indemnification

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=13937

Refer to the Directive on Claims and Ex Gratia Payments

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15782

Human Resources and Skills Development Canada

Refer to the Policy on Claims and Ex gratia Payments

Claims against the Crown – Canadian Human Rights Tribunal Awards (Column 10)

The authority to authorize payment of a claim obtained by a claimant through a Canadian Human Rights Tribunal Award.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Directive on Claims and Ex Gratia Payments

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15782

Human Resources and Skills Development Canada

Refer to the Policy on Claims and Ex gratia Payments

Conferences (Column 11) – some restrictions apply

This is the authority to approve conference attendance and sponsorship at departmental expense. Conference sponsorship and attendance should be directly related to the government objectives. Where feasible, consideration should be given to coordinating participation to ensure that the Government of Canada is not over-represented and thus subject to public criticism. The provisions of the Treasury Board’s Hospitality Policy and Travel Directive continue to apply to conferences sponsored by the department.

Conferences sponsored by departments and agencies should use the most economical location and preferably existing government facilities. In all cases, adequate provision must have been made in the department’s budgets before conference sponsorships are initiated.

All sponsorship of conferences and attendance must be pre-authorized by an officer with delegated authority and must be approved in accordance with applicable departmental policies. Particular care should be taken when approving attendance at conferences outside Canada to ensure participation and the number of attendees is appropriate and justified. For approval of travel associated with conference attendance, refer to Column 22 Travel.

Other Reference Material

Human Resources and Skills Development Canada

Refer to the Conferences Policy

Refer to the departmental Conferences Restrictions Document

[hyperlink not available yet]

Ex Gratia is a benevolent payment made by the Crown.

An ex-gratia payment is "accorded as a matter of grace, favor or indulgence, as distinguished from a payment that may be demanded as a matter of right.

An ex gratia payment is one for which no liability is recognized, whether or not any value or service has been received, that is made as an act of benevolence in the public interest (e.g. compensation for personal losses while on duty or compensation for damages, for which the Crown is not liable).

Prior to an ex gratia payment being made, it is imperative that all other compensation sources are reviewed, i.e. statutory or regulatory schemes, other Treasury Board policies, program funding, grants and contributions. After the review, when there is no other source of funds, no liability on the part of the Crown, and no restriction imposed on the existing schemes that would prohibit it, payment may be made ex gratia.

Judgment: Is a decision rendered by the courts to resolve a claim between respective parties.

Settlement: Is an agreement reached through negotiation between respective parties to resolve a claim.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Directive on Claims and Ex Gratia Payments

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15782

Human Resources and Skills Development Canada

Refer to the Policy on Claims and Ex gratia Payments

Hospitality (Column 13) – some restrictions apply

The Minister and Deputy Minister/Chairperson may delegate their authority to extend hospitality for specific occasions. Hospitality includes provision of meals, refreshments, and in exceptional circumstances, entertainment, to non-government persons and within certain criteria, government employees for matters related to conduct of official HRSDC business.

All hospitality provided must be pre-authorized by an officer with delegated signing authority and must be approved in accordance with the TB Hospitality Policy and applicable departmental orders, policies and directives.

If an employee attends a function from which he/she benefits personally, authorization must be obtained from his/her supervisor.

The manager should use government-owned facilities when they are appropriate and available.

Non-alcoholic refreshments can be offered to public servants in a formal gathering or when the dispersal of participants during a break period is undesirable.

Managerial discretion should be exercised in ensuring that hospitality is not offered during meetings of close colleagues working together on a regular basis.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Travel Directive

Travel Directive - Effective April 1, 2008 - Part 1 of 19

Refer to the Hospitality Policy

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12190

Human Resources and Skills Development Canada

Refer to the Hospitality Policy

Hospitality Policy

Refer to the departmental Hospitality Restrictions Document

[hyperlink not available yet]

Refer to the HRSDC Hospitality Procedures

Membership Fees (Column 14) – some restrictions apply

This is the authority to authorize the payment of a membership fee for departmental employees and corporate memberships.

The Treasury Board Membership Fees Policy requires that membership fees are only paid when departmental membership in a particular organization is in direct support of a departmental program or when membership is a federal statutory requirement for individual employees to carry out the functions of their positions. The policy covers all types of memberships, registration and licensing fees.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Chapter 6-1 Membership fees Policy

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12221

Human Resources and Skills Development Canada

Refer to Membership Fees Policy

http://iservice.prv/eng/finance/policies/membership.shtml

Refer to the departmental Membership Fees Restrictions Document

[hyperlink not available yet]

Refers to validation through demonstrated appreciation, to acknowledgement and, in some cases, to awards. Recognition covers a range of formal and informal practices in the workplace that collectively express and reinforces values and the way that people work together.

Recognition Awards - Informal (Column 15)

Informal recognition refers to everyday issues of trust, self-worth and working relationships with others. Informal recognition is extremely important in fostering pride, but is often overlooked. This type of recognition supports an employee's identification with the organization and its mission, and provides a foundation for formal recognition.

Day-to-day recognition is the act of acknowledging, on an informal and regular basis, the worth, quality and value of employee/team contributions that further the achievement of the Department's mission and/or goals. Pride and Recognition (informal) - Expenditures for awards and gifts provided under the "day-to-day" and informal components of the Pride and Recognition program in the context of recognizing attributes and behaviors that promote departmental values. Awards of appreciation include items such as pens, cards, plaques, frames, gifts from iBoutique.ca and other awards at the discretion of the RC manager. (Gifts may be taxable). Includes expenditures for frames bought for the Departmental Pride and Recognition Award certificate (the frame is not taxable).

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Recognition Policy

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12558

Human Resources and Skills Development Canada

Refer to Service Canada Pride and Recognition Program

Recognition and Awards – Formal (Column 16)

Authority to extend formal recognition to an employee for meritorious performance in the form of a sum of money, a citation, a certificate or any other type of recognition, including an Award of Appreciation.

Formal recognition refers to structured, scheduled activities (for example, the Awards of Excellence, National Public Service Week) and departmental-level recognition events. The credibility and integrity of formal recognition programs within organizations and institutions are crucial.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the Recognition Policy

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12558

Human Resources and Skills Development Canada

Service Canada Pride and Recognition Program

Relocation (Column 17) – some restrictions apply

This is the authority to approve relocation and sign documents initiating the expenditure of funds for relocation of members and employees or new appointees, and both the employer-requested and the employee-requested relocations. All relocation and relocation advances must be approved in accordance with TB policy, and other departmental authorities.

Reimbursements will be made to the employee or via the Third Party Service Provider, as per pre-negotiated agreement that is based on the National Joint Council (NJC) Relocation - Integrated Relocation Program (IRP) Directive and the Travel Directive.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to Policies, National Joint Council (NJC) Integrated Relocation Directive

http://www.njc-cnm.gc.ca/directive/nrd-drc/index-eng.php

Human Resources and Skills Development Canada

Refer to Departmental Policy on Relocation

Refer to the departmental Relocation Restrictions Document

[hyperlink not available yet]

Isolated Post & Government Housing (Column 18) – some restrictions apply

This is the authority to authorize isolated post assignments which are designed to facilitate the recruitment, retention and deployment of a satisfactory number and quality of staff to serve the employer's need in isolated locations.

It refers to additional benefits available to public servants who occupy positions in locations, which are deemed by Treasury Board to be "Isolated Posts". Isolated Post is governed by the Treasury Board Secretariat (TBS), Isolated Post Directive.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to Policies, Isolated Posts and Government Housing Directive

http://www.tbs-sct.gc.ca/psm-fpfm/pay-remuneration/other-autres/ipgh-pile/index-eng.asp

Refer to the departmental Isolated Post & Government Housing Restrictions Document

[hyperlink not available yet]

Staffing Action, Extra Duty (Column 19)

Authority to request for the classification of a position and/or the hiring of permanent, seasonal, part-time, term or casual staff. This excludes the hiring of temporary help services, which is covered through contracting.

Managers have authority to sign expenditure initiation documents for:

- appointments and classification

- extra duty pay

- acting pay

- leave payment authority

- emergency salary advances

- benefits

for their own areas of responsibility, within budgetary limitations and the delegation of Personnel Management Authorities, personnel policies and the terms of collective agreements. Where HRSDC pays a commercial entity for the provision of training and/or seats at a course, the agreement is considered a contract for services and all contract regulations and contract authority delegations must be respected.

Authority to authorize extra duty (overtime) work of an employee includes associated allowances (e.g. meal allowances) and other personal costs which are in addition to regular salary and wage.

The manager who exercises this authority must be aware of the restrictions in the acts, regulations, directives and collective agreements related to personnel matters. The local personnel office should be contacted for assistance and advice.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to Policies, Compensation and Pay Administration

Refer to Directive on Financial Management of Pay Administration

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15781

Human Resources and Skills Development Canada

Refer to Compensation & Benefits

Authority to authorize an accountable advance to an employee for the following purpose:

- travel, relocation and posting;

- establishing a deposit account;

- establishing a change fund;

- establishing a petty cash or other imprest fund.

Treasury Board of Canada Secretariat

Refer to Directive on Accountable Advances

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15789

Human Resources and Skills Development Canada

Refer to Departmental Policy on Accountable Advances

Authority to authorize the attendance of an individual at a training course or seminar and to incur the related expenses.

Learning is a shared responsibility between the individual and an obligation on the part of employees to take charge of their professional development and an obligation on the part of the organization to offer an environment that is conductive to learning.

All training must be pre-authorized by the supervisor and/or the manager of the employee.

Special Provisions for Courses with Canada School of Public Service (CSPS):

All training currently taken through the CSPS requires an Interdepartmental Letter of Agreement (ILA). The approval authority for ILAs (under Inter-Departmental Arrangements and Arrangements with Other Federal Institutions (Column 3)) is restricted to DG level and Director CFOB. The purpose of this delegation is to ensure the department has control over substantive expenditures or commitments of departmental resources made through inter-departmental arrangements.

To facilitate the efficient authorization of training, the Chief Financial Officer of HRSDC has authorized the following:

- For individual employee training, the delegation for Training/Tuition (column 21) is the delegation to utilize for approving both the training and the ILA.

- For group training up to $5,000, the delegation for Training/Tuition (column 21) is the delegation to utilize for approving training, but the ILA must be approved at the Director level or above.

- For group training over $5,000, the delegation for Training/Tuition (column 21) is the delegation to utilize for approving training and the delegation for Inter-Departmental Arrangements and Arrangements with Other Federal Institutions (Column 3) is the delegation to utilize for approving the ILA.

Note that all processes in place from the Service Canada College and branch/regional management must be respected.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to Policy on Learning, Training, and Development

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12405

This is the authority to approve the travel of Public Service employees, exempt staff and other persons travelling on government business. Business travel includes trips to attend training, conferences and meetings. All travel must be pre-authorized by the manager of the traveler. The expenses incurred by the traveler while on travel status will be paid or reimbursed as prescribed in the Treasury Board Travel Directive and Special Travel Authorities.

Emphasis is put on the importance of close consultation between employees and managers in planning and determining travel arrangements that best accommodate their respective needs. Within his/her delegated signing authority, the traveler’s manager has the following responsibilities:

- Ensure that travel arrangements are consistent with the provisions of the directive

- Authorize travel

The manager also has the responsibility to verify and approve travel expense claims for his/her subordinates before reimbursement.

The Travel Authorization and Advance Form (FIN5030) (opens new window) must be filled out and approved prior to the start of the business travel.

Employees on government business travel shall utilize government-approved suppliers, services and products selected in support of government business travel when these are available.

Government hotel directories shall serve as a guide for the cost, location and selection of accommodation.

Unless it is under special circumstances, it is recommended that the individual Travel Card be used as much as possible, especially for the frequent travelers.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to Travel Directive

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=13856

Refer to Directive on Travel Cards and Travellers Cheques

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15783

Human Resources and Skills Development Canada

Refer to Departmental Policy Travel Modernization - New Travel Directive

Travel Modernization

Refer to Departmental International Travel Policy

http://iservice.prv/eng/finance/policies/intrnatnltravel.shtml

Contracting Authority (Column 23) – some restrictions apply

This is the authority to enter into contracts. Contracting is a rather complex area which is beyond the scope of these Explanatory Notes. For enquiries please contact a Procurement & Contracting specialist.

Other Reference Materials

Public Works and Government Services Canada

Refer to Customer Manual, Chapter 120

http://www.tpsgc-pwgsc.gc.ca/

Treasury Board of Canada Secretariat

Refer to Contracting Policy

http://www.tbs-sct.gc.ca/pubs_pol/dcgpubs/Contracting/contractingpol_e.asp

Refer to Directive on Acquisition Cards

Human Resources and Skills Development Canada

Refer to Contracting and Procurement Policy

Contracting and Procurement

Refer to the departmental Contracting Restrictions Document

[hyperlink not available yet]

Leasing Authority (Column 24) – some restrictions apply

The Treasury Board Policy on Management of Real Property (Appendix B) sets departmental limits on departmental leasing authority above which Treasury Board approval must be sought. All enquiries and questions concerning real property management, including leases and other matters covered by the Federal Real Property Act and its Regulations, may be directed to the Procurement & Contracting, CFOB.

Treasury Board of Canada Secretariat

Refer to the Management of Real Property Policy

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12042

FAA Section 34 Contract Performance (Column 25)

Section 34 of the FAA is the authority to certify that work has been performed as required; services and supplies have been satisfactorily provided; travel and relocation have been successfully carried out (subject to pre-audit of relocation travel claims and invoices by the purchasing organization); employee overtime has been worked and contract performance has been completed in accordance with contractual terms and conditions or is reasonable. This authority is also used to certify that terms and conditions/eligibility have been met for the payment of grants and contributions.

This also includes the authority delegated to appropriate officers to certify under Section 34(b) where a payment is to be made before completion of the work as it is so stated in the contract.

Primary responsibility to perform account verification on all payments and settlements rests with managers who are delegated the authority to certify under Section 34 of the FAA.

No manager shall exercise Section 34 of the FAA with respect to a payment from which he or she personally can benefit, directly and indirectly.

This certification is a prerequisite to requisitioning a payment.

RCMs are responsible and accountable for the correctness of payment requests and ensuring all account verification procedures are carried out.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to Directive on Delegation of Financial Authorities for Disbursements

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=17060

Refer to Directive on Account Verification

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15790

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

FAA Section 33 Payment Authority (Column 26)

This authority cannot be exercised unless Section 34 has been exercised.

This authority is normally delegated to financial officers to requisition payments for charges against appropriations whether they are from a departmental bank account or via the department’s integrated financial system. This is done after reviewing the legality of payments before they are requisitioned and exercising all appropriate financial controls. Financial officers must also provide assurance of the adequacy of the Section 34 of the FAA account verification and be in a position to state that managers are properly and conscientiously following the process in place.

Exercising payment authority involves ensuring:

- The charge is a legal charge against the appropriation

- Expenditures in excess of the appropriation will not result from the payment

- Expenditures do not reduce the balance available in the appropriation to a level where previous commitments charged against it cannot be met.

No person shall exercise signing authority for both Sections 33 (payment) and 34 (contract performance) of the FAAfor a particular payment.

No person shall be permitted to exercise spending or payment authority for a payment, which that person may personally benefit.

The Standard Payment System (SPS) requires an electronic signature for Section 33 of the FAA. The “Electronic Authorization and Authentication” (EAA) signature is created to authorize a Financial Officer to exercise Section 33 of the FAA through the PWGSC Mainframe.

It is the responsibility of the DG Corporate Accounting and Financial Reports to designate the financial officer positions authorized to transmit the departmental trial balance to PWGSC.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to Directive on Delegation of Financial Authorities for Disbursements

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=17060

Refer to Directive on Account Verification

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15790

Refer to Directive on Payment Requisitioning and Cheque Control

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15784

Department of Justice Canada

Refer to Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

DELEGATION CHART - SPECIAL FINANCIAL AUTHORITIES

This delegation chart is for special approval authority.

Accept and Release Security Deposit (Column 1)

This is the authority to authorize the acceptance of any security in respect of a debt or obligation due or payable to the department or a claim by the department. Security deposits are deposits pledged to the department as security in the case that a default on a contract, permit or agreement occurs.

The deposit should be in accordance with the contract, agreement, permit and/or legislation giving rise to the deposit and it must be a legal, valid and original document (e.g., cheque, expiry date, properly certified; if a bond is used, the department must ensure that it is listed in the annual TB Circular which lists “Acceptable Bonding Companies”).

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to Treasury Board Circular 1989-2, Policy Related to the Regulations Governing Security for Debts Due to Her Majesty

Regulations Governing Security for Debts Due to Her Majesty - TB Circular 1989-2

Refer to Directive on Receipt, Deposit and Recording of Money

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15785

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

Bid/Contract Security (Column 2)

The Departmental Security Policy and Procedures Manual contains the security requirements and guidelines, simplified for use by directors, managers and employees.

Included in the Manual are sections on Information Security, Emergency Response, Partnerships and Alternate Service Delivery, Telework and Business Continuity Planning.

Directors and managers are encouraged to familiarize themselves and their staff with the Manual and make use of it as an operational reference.

The Government Security Policy (GSP) requires that all employees and contractors who have access to sensitive information, assets and facilities be subject to a security screening. This includes consultants, maintenance and other outside services which may have unsupervised access to the offices.

Because of the nature of the business, the department requires that all employees and contractors undergo a Reliability Status (RS). Regardless of the duration of employment or the contract, when the duties of the position or the work description require access to sensitive information and assets, a RS must be completed before work can commence.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to the policy of Contracting Policy

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=14494

Refer to TB Framework for the Management of Assets and Acquired Services

http://publiservice.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12022

Cash Loss Charge-off to Appropriation (Column 3)

This authority includes all losses of money, however caused, as well as offences against the Crown and improprieties that involve money or public property - whether committed by employees, contractors or other suppliers.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to Directive on Losses of Money or Property

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15792

Human Resources and Skills Development Canada

Refer to Policies, Policy on Losses of Money and Illegal Acts Against the Crown

Cheque Issue Regulation – DBA (Column 4)

This authority is normally delegated to financial officers to requisition payments for charges against appropriations whether they are from a departmental bank account or via the department’s integrated financial system. This is done after reviewing the legality of payments before they are requisitioned and exercising all appropriate financial controls.

It is departmental policy to use the Receiver General’s Standard Payment System (SPS) priority payment process for emergency cheque issue. The use of DBAs is restricted to emergency situations where no other reasonable alternative exists.

A Zero-balance account is a departmental bank account used in Canada and funded in Canadian dollars. The Receiver General sets up these accounts in the name of a department with a financial institution in Canada. These accounts are only used to issue cheques for authorized classes of payments.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to Directive on Departmental Bank Accounts

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15791

Refer to the Directive on Account Verification Policy

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15790

Refer to Directive on Payment Requisitioning and Cheque Control

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15784

Human Resources and Skills Development Canada

Refer to the Policy on Departmental Bank Accounts

http://iservice.prv/eng/finance/policies/setoff.shtml

Deduction and Set-Off of Accounts – (Column 5 to 7)

This is the authority to authorize the retention or collection of the amount of indebtedness by way of deduction from or set-off against any sum of money that may be due or payable by Her Majesty in right of Canada to the person or the estate of that person.

Deduction and Set-Off of Accounts – HRSDC Programs (Column 5)

This authority is in regard to indebtedness within and between HRSDC programs and NHQ.

Authorize Deduction and Set-Off: Pursuant to Subsection 155(1) of the FAA, is the authority to retain any amount of indebtedness to Her Majesty in right of Canada for which the Minister is responsible to recover or collect by way of deduction from or set-off against any sum of money due or payable by Her Majesty in right of Canada to the debtor or the estate of the debtor.

Consent to Deduction and Set-Off: Pursuant to Subsection 155(4) of the FAA, is the authority to consent to the retention of any amount of indebtedness to Her Majesty in right of Canada for which another Minister is responsible to recover or collect by way of deduction for or set-off against any sum of money due or payable by HRSDC to the debtor or the estate of the debtor.

Other Reference Materials

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

Deduction and Set-Off of Accounts – Other Government Department (OGD) (Column 6)

This authority is in regard to an indebtedness to or from another federal department or agency.

Other Reference Materials

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

Deduction and Set-Off of Accounts – Salary of Current employees (Column 7)

This authority is in regard to an indebtedness of a current NHQ or regional HRSDC employee.

Other Reference Materials

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

Human Resources and Skills Development Canada

Refer to the policy on the Set-Off of Debts Owed to the Crown

http://intracom.hq-ac.prv/en/cfob/policies/setoff.shtml

This is the authority to authorize that a sum of money be withheld from an employee’s pay cheque and subsequently be forwarded to the specified court upon receipt of a garnishee summons.

This authority allows under the Garnishment Attachment and Pension Diversion Act for the garnishment of salaries and other remuneration paid to government employees, as well as for the garnishment of fees paid to a contractor engaged as an individual (as opposed to a corporation) under contract for services only.

Other Reference Materials

Treasury Board of Canada Secretariat

Refer to the Policy on Garnishment

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12138

Department of Justice Canada

Refer to Garnishment, Attachment and Pension Diversion Act

http://laws.justice.gc.ca/en/G-2/index.html

Authority to Fix Travel and Living Expenses of PAB Temporary Members (Column 9)

This delegation provides the authority to fix the amounts of the travel and living entitlements to be paid to the Pension Appeals Board Temporary Members as related to the performance of their duties and functions under the Canada Pension Plan Act.

Other Reference Materials

Department of Justice

Refer to the Canada Pension Plan Act

http://laws-lois.justice.gc.ca/eng/acts/c-8/index.html

Refund of Revenue (FAA s.20) (Column 10)

This is to authorize the refund of money received for any purpose that is not fulfilled or money that is not public money.

Other Reference Materials

Department of Justice Canada

Refer to the Financial Administration Act

http://laws-lois.justice.gc.ca/eng/acts/f-11/

Treasury Board of Canada Secretariat

Refer to Directive on Receivables Management

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=17063

Transaction Against the Annuities Account (Columns 11 and 12)

The purpose of the Government Annuities Act was to assist individuals and groups of Canadians to prepare financially for their retirement by purchasing government annuities. In 1975, the Government Annuities Improvement Act discontinued future sales of Government Annuity contracts. Annuities are deferred until their maturity date, at which time payments to annuitants begin. The Account is administered by Human Resources and Skills Development Canada and operated through the Consolidated Revenue Fund.

Receipts and other credits consist of premiums received, funds reclaimed from the Consolidated Revenue Fund for previously untraceable annuitants, earned interest and any credit needed to cover the actuarial deficit. Payments and other charges represent matured annuities, the commuted value of death benefits, premium refunds and withdrawals, and actuarial surpluses and unclaimed items transferred to non-tax revenues. The amounts of unclaimed annuities, related to untraceable annuitants, are transferred to non-tax revenues.

Other Reference Materials

Public Works and Government Services Canada

Refer to the Public Accounts

http://www.tpsgc-pwgsc.gc.ca/recgen/cpc-pac/index-eng.html ![]()

Treasury Board of Canada Secretariat

Refer to the Directive on Recording Financial Transactions in the Accounts of Canada

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15793

Transaction Against the Civil Service Insurance Account (Columns 13 and 14)

This account was established by the Civil Service Insurance Act, introduced to enable the Minister of Finance to contract with a person appointed to a permanent position in any branch of the public service, for the payment of certain death benefits. No new contracts have been entered into since 1954, when the Supplementary Death Benefit Plan for the Public Service and Canadian Forces was introduces as part of the Public Service Superannuation Act and the Canadian Forces Superannuation Act, respectively. As of April 1st, 1997, the Department of Human Resources and Skills Development assumed responsibility for the administration and the actuarial valuation of the Civil Service Insurance Act.

In support of its responsibility, management has developed and maintains books of account, financial and management controls, information systems and management practices. These are designed to provide reasonable assurance as to the reliability of the financial information, and to ensure that the transactions are in accordance with the Employment Insurance Act and regulation, as well as the Financial Administration Act and regulation.

Other Reference Materials

Public Works and Government Services Canada

Refer to the Public Accounts

http://www.tpsgc-pwgsc.gc.ca/recgen/pdf/49-eng.pdf

Treasury Board of Canada Secretariat

Directive on Recording Financial Transactions in the Accounts of Canada

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15793

Transaction - Annuities Agent (Columns 15 and 16)

This authority is related to Annuities Agents’ Pension Account. This account was established by Vote 181, appropriation Act No. 1, 1961, to provide pension benefits to former eligible government employees who were engaged in selling government annuities to the public.

Other Reference Materials

Public Works and Government Services Canada

Refer to the Public Accounts

http://www.tpsgc-pwgsc.gc.ca/recgen/pdf/49-eng.pdf

Treasury Board of Canada Secretariat

Directive on Recording Financial Transactions in the Accounts of Canada

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=15793

Write-Off of Crown Assets (Column 17)

This is the authority to authorize an adjustment to the inventory record for an asset that is disposable or not available, as well as approve the disposal of the asset.

This is the authority to delete records of materiel due to inventory shortage, destruction, fire, theft, loss and other reasons. This refers to both equipment in use and to materiel held in stores.

Managers should recommend write-off or disposal to the appropriate departmental level, but managers should not have the authority to write-off or dispose of materiel for which they are directly responsible.

Materiel management maintains records to control the department's materiel and to record the write-off materiel. Materiel losses due to theft should be reported immediately to security and local police authority.

Other Reference Material

Treasury Board of Canada Secretariat

Refer to Policies, Policy Framework for the Management of Assets and Acquired Services

http://www.tbs-sct.gc.ca/pol/doc-eng.aspx?id=12022